My relationship with money hasn’t always been easy. I didn’t grow up in a family that had a lot of money. We lived in a rural Canadian town. My dad was a construction worker and my mom worked at a local plant for part of the year. A budget wasn’t something that was ever discussed, or even heard of, since we lived paycheck to paycheck.

My dad had some pretty bad habits that sucked up a lot of his paycheck, and as the primary breadwinner, we then felt this on down the line. My mom made do with what resources she had and she did a great job covering our basic needs. She grew vegetables in a garden that she would store in our cellar during the winter. She’s a fantastic cook and baker so there was always fresh bread and we had a big feast every Sunday.

Luckily, we lived in a rural area where the cost of living was low and we spent most of our days outside playing. It was a pretty decent childhood. But I didn’t learn anything about managing money and school definitely didn’t teach it to me. All I ever saw was that you spent what you had. And as I became a teenager, I started to realize all of the things that I couldn’t have which put me in a constant state of want.

It should come as no surprise that I needed student loans for college. And what did I do when that money hit my bank account for the first time? I hit up the local mall. And so started a horrible relationship with money, one where I blew any money not tagged for bills on clothes. One where I took on debt to live a life I couldn’t afford.

And it took me a lot of years to break out of this pattern.

I started to actively budget over a decade ago, even in the depths of my shopping addiction. I knew I had a problem and I tried for many years to fix it. Becoming more conscientious about my shopping helped me get over being a shopaholic, which ultimately helped me have a healthier relationship with money.

Even today, my budget isn’t always pretty and I’ve gone over budget probably as much as I’ve stayed under, but I’m a work in progress.

Lately, I’ve been using a system that works for us pretty well. I like to work with a monthly system, but you could apply the same steps to a weekly or bi-weekly budget.

1. Calculate income for the month.

This includes money from work and any other streams of income that you know of.

2. Calculate all necessary expenses for the month.

Include bills such as mortgage/rent, car payments, and utilities. Include any additional debt payments here as well.

These are the things that you are contractually obligated to pay or the things that you need to live comfortably such as heat, light and water.

It is best to have this number be less than 50% of your income.

Food is also a need, but I will include that later as it is not a fixed cost and can be increased or decreased as desired or needed.

3. Calculate all savings for the month.

This includes any savings goals that you have. This could be for a house downpayment, a college fund, a vacation fund or at the very least, an emergency fund.

A good rule of thumb is to save 20% of your income. I know this is not always possible depending on where you live, but try to put a little back each month to cover any emergencies.

4. Subtract your savings and expenses from your income.

The amount that you have left is your disposable cash.

This is the money that will cover the things that you spend money on because you enjoy them (such as subscription services or memberships) or expenses that aren’t set month to month (such as groceries, gas, dining out, household expenses, including laundry detergent, cleaners, bath and beauty products, hair care, pet care and general spending money).

5. Calculate all unnecessary expenses such as monthly subscription services or club memberships.

Include anything that you like to spend money on because you enjoy it that has a fixed fee each month. Include such things as internet, cell phone service, gym membership, and video streaming services here.

These are the things that you could easily let go of if you were in financial hardship.

You may argue that a cell phone is a necessity and I wouldn’t disagree. But an expensive cell phone plan isn’t.

You may also argue that internet is a necessity but you can do anything sensitive, such as banking, on your phone and the local library or mall has free wi-fi for anything else.

6. Subtract unnecessary spending from your disposable cash.

7. Divide your remaining disposable cash amount by 4.35.

This is the average number of weeks in a month. The amount that you get is your weekly allowance.

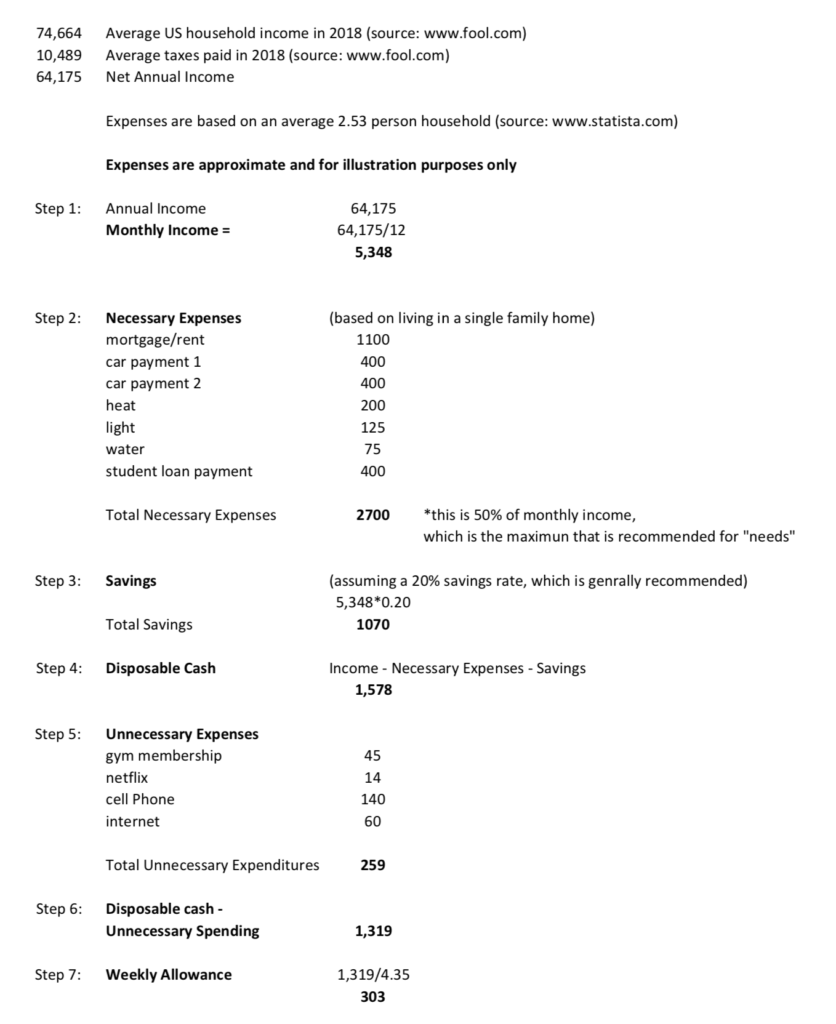

Example Budget

The following is an example of a budget using the method outlined in the above 7 steps. It is based on an annual net income of $64,175 or $5,348 per month.

8. Set up a tracking system.

One of the easiest ways to track your spending is to get a piece of paper and divide it into weeks.

Make it a page in your monthly planner or put it somewhere visible (sticking it to your fridge is a good place). At the end of each day, record any money you (or anyone in your family) spent that day.

9. Calculate your total expenditures at the end of the week.

Make adjustments as needed. If you went over by $20, subtract $20 from next week. If you were under budget by $20, add that to your savings or move it to next week.

And that’s it! I find it easy to keep track of the money I’m spending on a weekly basis so this has been the best budgeting system I’ve found that works for me.

Do you have a budget system? I’d love to hear what works for you.

And if you don’t have a current system, will you try mine?

Until next time,